Vaccinations & Rotations

Only a fraction of investors would have assumed on March 23rd that there would be more companies worth over a trillion dollars in market capitalisation than there were prior to the pandemic, and the likes of Tesla surging over 600% in 2020. This illustrates the importance of active selection. The question we now face is are we about to see an alternation?

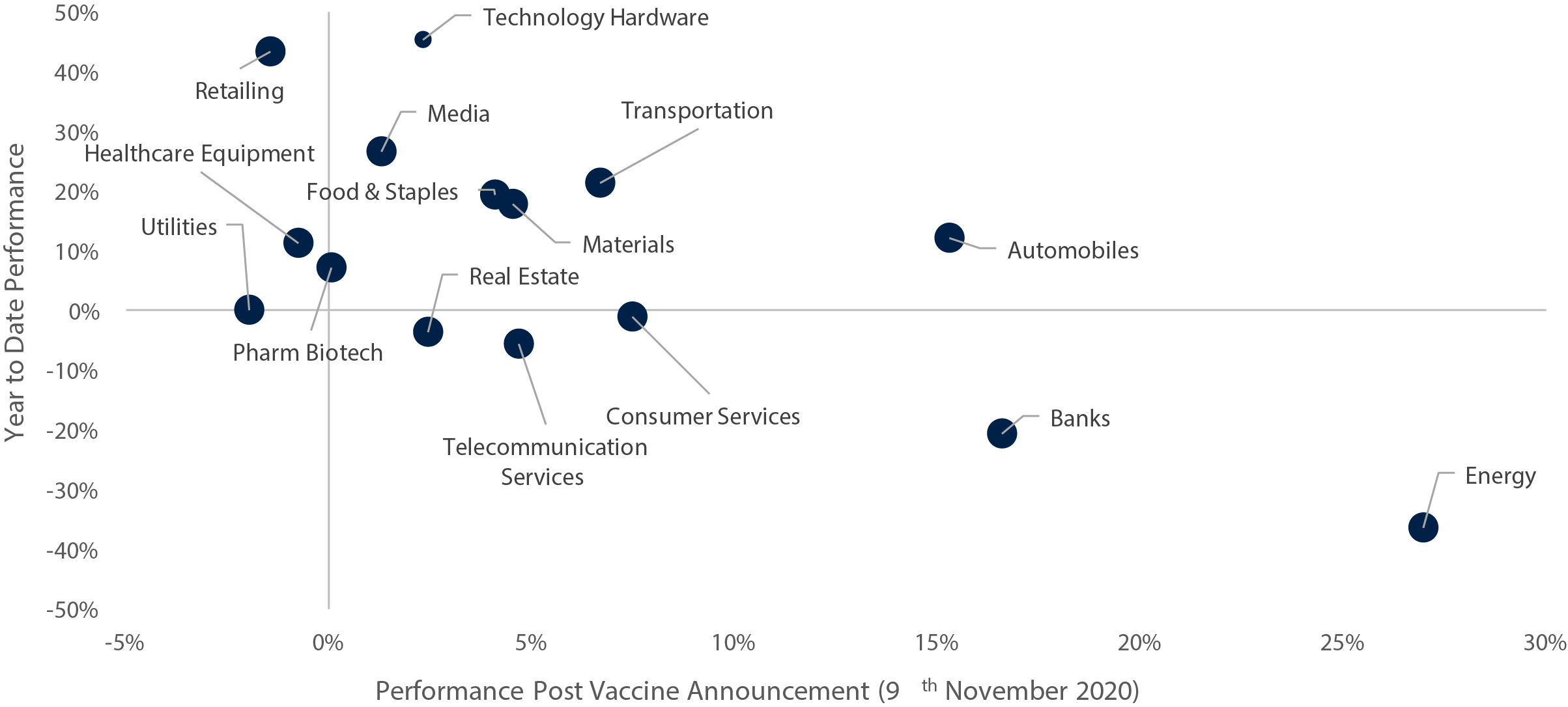

The announcement of three effective vaccines and a standout US election result propelled markets into a style rotation throughout November. Investors shifted out of their 2020 winners, namely US technology stocks that have extended to all-time highs on the backdrop of low interest rates and unprecedented fiscal & monetary stimulus, into this year’s less favourable areas, namely value and cyclical sectors on the expectation of a return to economic normality.

The positioning into the 2020 laggards is understandable, as the bias towards growth stocks this year such as technology has been far from ambiguous, with tech ETF’s witnessing their largest inflows since the height of the dotcom era, and the S&P 500 Growth Index outperforming its counter Value index by 30% year to date. The consensus of the “stay at home” trade has witnessed the Nasdaq rally 76% from its nadir on March 23rd and return 42% year to date, helped by stocks such as Zoom and Microsoft that have seen a surge in usage of their video facilities as employees work from home.

Though, not all sectors have been as fortunate, Banks and Energy specifically have had a gruelling year. US Banks have been instructed not to provide dividends in the face of scarce liquidity, and this was the first year that an oil future contract went negative. Despite this, the vaccine announcement led a rally in November, with US energy stocks rising 27% and US Banks climbing 17%.

Nevertheless, the US energy index remains down -37% year-to-date, whilst the US Bank composite is down -21%. The lacklustre demand in oil and low interest rate environment have been headwinds for these sectors throughout 2020, but recent optimism for a rebound in economic growth in 2021 may lead a comeback for these laggard sectors next year.

However, with the Federal Reserve set to keep rates anchored, inflation suppressing real rates, and concerns surrounding vaccine distribution, their recent outperformance may be unsustainable. Governments will have to sober their view on their expanding debt load, whilst central banks will have to remain vigilant in avoiding a policy error on when to turn off the liquidity taps. The bill always comes due, and with so many risks for markets to face, 2021 is set to be another interesting year.

The Vaccine Impact on S&P 500 Sector Returns

Equity Returns

h3 >

Fixed Income Returns

h3 >

Commodities & FX Returns

h3 >

Source: Signia Wealth, Bloomberg. Data as at 30/11/2020. Global Equities: iShares MSCI ACWI ETF; Global Aggregate: Vanguard Global Bond Index GBP Hedged Fund; Global Sovereign: Xtrackers Global Government Bond GBP Hedged ETF; Global IG Corporate: Vanguard Global Corporate Bond Index GBP Hedged Fund; Global HY Corporate: iShares Global High Yield Corporate Bond GBP Hedged ETF; EM$ Sovereign: iShares J.P. Morgan USD EM Bond ETF; EM$ Corporate: iShares J.P. Morgan USD EM Corporate Bond ETF; EM Local Sovereign: iShares J.P. Morgan EM Local Government Bond ETF.

Equities

• European and Japanese equities rose sharply in November, as hopes for a Covid-19 vaccine spurred cyclical stocks to outperform

• UK and US indices also achieved strong positive returns on the vaccine news, though UK equities continued to be affected by Brexit uncertainty

• Chinese equities lagged their developed market counterparts, as profit taking and the prospect of greater regulation weighed on gains

Jack Rawcliffe

Fixed Income

• Despite finishing the month in positive territory, the global sovereign bond index underperformed risky assets as risk-on sentiment was spurred by the US election results and the encouraging news flow surrounding COVID19 vaccine trials.

• Global corporate credit spreads tightened on the back of the vaccine trials, a more propitious environment for credit given the reduced probability of a “blue wave” democratic sweep at the US elections, and continued support from central banks, leading to the second and third strongest month for global high yield and global investment grade credit respectively.

• Emerging market debt followed suit as improved global risk sentiment and positive data releases from China saw all three major emerging market debt sub-indices generate strong performances this month.

Grégoire Sharma

Commodities & FX

• WTI Crude surged 26.7% posting its first gain since August, as investors anticipated a return to demand following the vaccine announcement.

• The rotation away from safe havens saw gold experience its worst monthly performance in 4 years (-5.4%). The precious metal is still up 19.6% YTD.

• The US dollar continued its bearish trend as it fell against most of its major counterparts, this saw EM and Commodity based currencies surge as investors took riskier positions.

Harry Elliman

Choose a Service to Invest through

United States of America

The US economy has rebounded quicker and stronger than expected over the summer after the shortest sharpest recession in history, which saw the economy contract -10.4% in nominal terms during the first half of 2020. However, coronavirus infections remain high and are rising again after the Thanksgiving holidays, and congress remains divided on further fiscal stimulus measures to help Main Street where small businesses are struggling.

Eurozone

Europe has experienced a deeper economic recession this year versus other regional economies and deflation risk is now gripping the regional bloc after four consecutive months of negative year-on-year CPI prints. Second economic lockdowns are still largely in force as winter covid infections persist, further pressuring inflation expectations, However, with the European Recovery Plan nearing ratification by all 27 EU states and additional ECB stimulus on the way in December, expectations for higher economic growth in 2021 and beyond are rising.

United Kingdom

The UK suffered a worse economic and humanitarian fate relative to the Eurozone after being slower to introduce coronavirus containment measures that were amongst the strictest in Europe. With November’s Lockdown 2.0 now finished and a return to stricter local tiered restrictions in place to counter still persistently high daily infection rates, an economic contraction in Q4 looks increasingly possible alongside a no-deal Brexit at the end of the year.

Japan

In his first months of leadership Prime Minister Suga has so far successfully navigated his country through the ongoing pandemic, avoiding any runaway second wave of infections in Japan in contrast to many of its northern hemisphere winter counterparts. Domestic economic growth indicators for 2020 are also outpacing most G10 counterparts, however with many structural issues in Japan persisting, namely demographic, the economic bounce for the Japanese economy next year is still expected to be relatively modest.

China

China is one of very few global economies that has avoided an economic recession this year by growing an impressive 4.9% year-on-year in the third quarter after quickly returning economic operating capacity back to pre-pandemic levels. Chinese GDP is expected to continue its solid growth path and rebound to its long-term historical growth rate of 8% in 2021. China’s recently announced new five-year economic plan elevates its self-reliance in technology into a national strategic pillar, most likely as a direct result of growing competitive tensions and trade wars with the US.

Emerging Markets

Emerging economies, mostly outside of Asia, are still feeling the full economic and humanitarian impact from the coronavirus crisis. Economic performance has been mixed this year with commodity producers Brazil and Russia suffering from a collapse in prices, India as a net importer of commodities benefitting from price declines but suffering badly from a protracted and damaging first wave on infections; and Taiwan and South Korea feeling less economic pain due to successful virus containment measures and buoyant trade tailwinds with China.

Important Information

The information set out in this document has been provided for information purposes only and should not be construed as any type of solicitation, offer, or recommendation to acquire or dispose of any investment, engage in any transaction or make use of the services of Signia. Information about prior performance, while a useful tool in evaluating Signia’s investment activities is not indicative of future results and there can be no assurance that Signia will generate results comparable to those previously achieved. Any targeted returns set out in this document are provided as an indicator as to how your investments will be managed by Signia and are not intended to be viewed as a representation of likely performance returns. There can be no assurance that targeted returns will be realised. An estimate of the potential return from an investment is not a guarantee as to the quality of the investment or a representation as to the adequacy of the methodology for estimating returns. The information and opinions enclosed are subject to change without notice and should not be construed as research. No responsibility is accepted to any person for the consequences of any person placing reliance on the content of this document for any purpose. No action has been taken to permit the distribution of this document in any jurisdiction where any such action is required. Such distribution may be restricted in certain jurisdictions and, accordingly, this document does not constitute, and may not be used for the purposes of, an offer or solicitation to any person in any jurisdiction were such offer or solicitation is unlawful. Signia Wealth is authorised and regulated by the Financial Conduct Authority.